25

Dimensionality Reduction

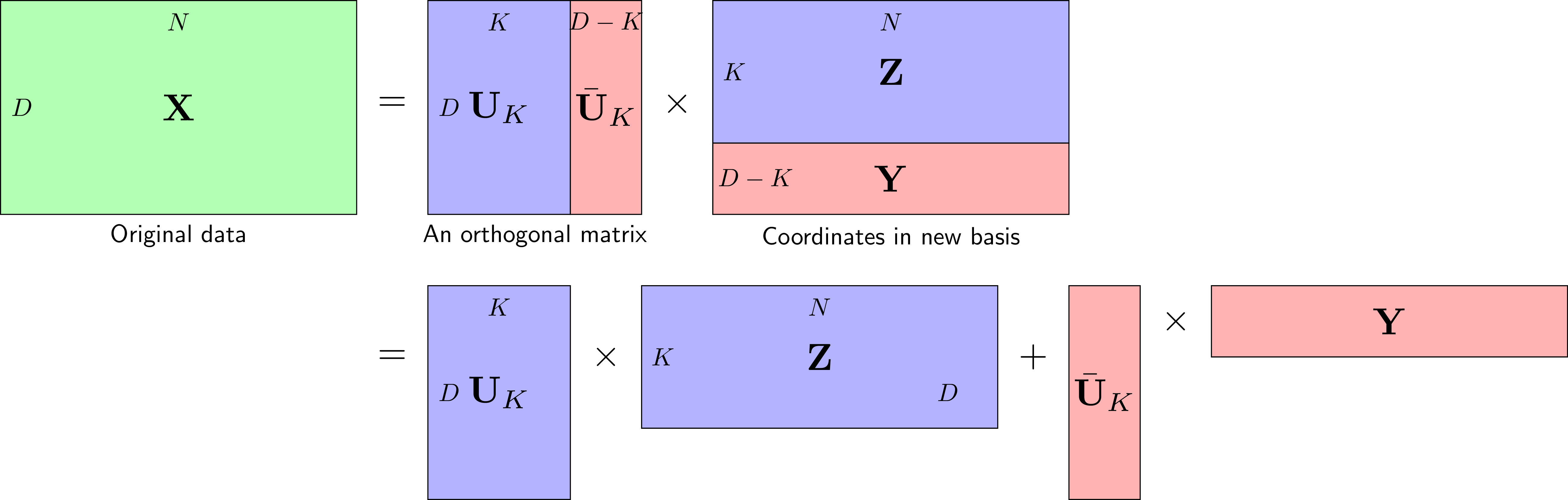

Principal Component Analysis (1/2)

Theory

PCA is a dimensionality reduction technique that transforms data into a new coordinate system where the greatest variance lies on the first coordinate (first principal component). It's unsupervised and finds directions of maximum variance.

Visualization

Mathematical Formulation

Algorithm: 1. Standardize data (mean=0, variance=1) 2. Compute covariance matrix C = XᵀX/(n-1) 3. Compute eigenvectors and eigenvalues of C 4. Sort eigenvectors by eigenvalues (descending) 5. Project data onto top k eigenvectors Key Properties: • PCs are orthogonal • First PC captures most variance • Equivalent to SVD on centered data

Code Example

import numpy as np

from sklearn.decomposition import PCA

from sklearn.preprocessing import StandardScaler

# Generate 3D data

np.random.seed(42)

mean = [0, 0, 0]

cov = [[3, 2, 1], [2, 4, 1], [1, 1, 1]]

X = np.random.multivariate_normal(mean, cov, 200)

print(f"Original data shape: {X.shape}")

print(f"Mean: {X.mean(axis=0)}")

# Standardize

scaler = StandardScaler()

X_scaled = scaler.fit_transform(X)

# Apply PCA

pca = PCA(n_components=2)

X_pca = pca.fit_transform(X_scaled)

print(f"\nPCA transformed shape: {X_pca.shape}")

print(f"Explained variance ratio: {pca.explained_variance_ratio_}")

print(f"Cumulative variance: {np.cumsum(pca.explained_variance_ratio_)}")

# Reconstruction

X_reconstructed = pca.inverse_transform(X_pca)

reconstruction_error = np.mean((X_scaled - X_reconstructed) ** 2)

print(f"\nReconstruction MSE: {reconstruction_error:.6f}")

# Scree plot data

pca_full = PCA()

pca_full.fit(X_scaled)

print(f"\nAll explained variance ratios:")

print(pca_full.explained_variance_ratio_)